Short answer: If an Uber Eats, DoorDash, or Grubhub driver hit you in Chicago, who pays depends on exactly what the driver was doing at the moment of the crash. Gig delivery platforms carry commercial insurance policies of up to $1 million while a driver is actively making a delivery. But if the driver was logged into the app without an active order, coverage drops significantly. If the driver was completely off-app, only their personal auto policy applies. Sorting out these overlapping coverage tiers is complicated, and insurers do not make it easy. An experienced Chicago car accident attorney can identify every available insurance policy and make sure you pursue the full compensation you are entitled to under Illinois law.

Why Food Delivery Driver Crashes Are More Complex Than Ordinary Accidents

I have represented Chicago injury victims in hundreds of car accident cases over the years, and gig economy delivery crashes are among the most complicated. The core problem is that Uber Eats, DoorDash, and Grubhub classify their drivers as independent contractors, not employees. That classification matters for insurance because it creates layered, conditional coverage that shifts depending on the driver’s app status at the moment of the collision. I have handled cases where the driver’s personal insurer immediately denied the claim because the driver was working at the time, while the gig platform simultaneously argued the driver was not actively on a delivery when the crash happened. That coverage gap can leave injured people struggling to get any compensation at all. This guide explains how the coverage tiers actually work in Illinois and what you need to do after a delivery driver hits you.

The Insurance Coverage Gap Problem

The coverage gap is the central issue in food delivery driver accident claims. Standard personal auto insurance policies explicitly exclude coverage when the vehicle is being used for commercial purposes. The moment a driver accepts a delivery gig, their personal policy may deny any crash that happens during that period.

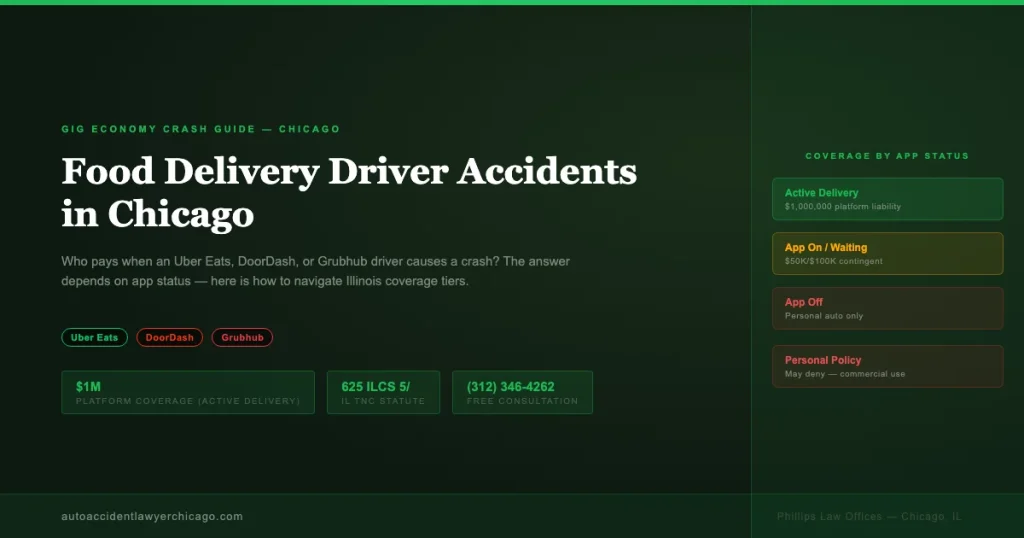

At the same time, gig platforms like Uber Eats and DoorDash only provide their full commercial coverage while a driver has accepted an active delivery order. In the period between when a driver logs into the app and when they accept a delivery request, coverage from the platform is limited. This gap is where many injured victims fall through the cracks.

The coverage gap is not accidental. Gig platforms designed their insurance structure to minimize payouts during the riskiest period of a driver’s shift. I have seen drivers log 50 miles cruising between delivery zones, all while carrying only contingent liability coverage. If they cause a serious crash during that window, injured victims may be dealing with a personal policy exclusion and a platform policy that pays a fraction of the damages. Getting legal counsel early is the only way to make sure every coverage layer gets properly claimed.

Coverage by Platform: Uber Eats, DoorDash, and Grubhub

Each major food delivery platform has its own insurance structure, but they all share the same basic three-tier model. The table below compares what each platform covers at each stage of a driver’s shift:

| App Status | Uber Eats | DoorDash | Grubhub |

|---|---|---|---|

| App off / driver not logged in | No platform coverage, personal auto only | No platform coverage, personal auto only | No platform coverage, personal auto only |

| App on, waiting for order (no active delivery) | $50K/$100K bodily injury; $25K property damage (contingent) | $50K/$100K bodily injury; $25K property damage (contingent) | Limited contingent coverage while waiting |

| Order accepted, en route to pick up food | $1M third-party liability; comprehensive/collision if driver carries it | $1M third-party liability; comprehensive/collision (if driver carries it) | $1M third-party liability coverage |

| Food picked up, delivering to customer | $1M third-party liability; comprehensive/collision | $1M third-party liability; comprehensive/collision | $1M third-party liability coverage |

Note: “Contingent” coverage means the platform’s policy only kicks in if the driver’s personal insurer denies the claim first. This adds another layer of delay and dispute to an already complicated process.

Illinois Law on Rideshare and Delivery Coverage

Illinois has specific statutes governing Transportation Network Providers under 625 ILCS 5/7-500 et seq. These laws require rideshare and delivery network companies operating in Illinois to maintain minimum insurance coverage at each phase of a trip or delivery. Key requirements include:

- During the period when a driver is logged into the app but has not yet accepted a request: at least $50,000 per person and $100,000 per accident for bodily injury, plus $25,000 for property damage

- From the moment a driver accepts a delivery through the completion of that delivery: at least $1,000,000 in coverage for death, bodily injury, and property damage

- Coverage must be maintained by the TNC (the platform) or by the driver, with the platform’s coverage primary during active delivery periods

Illinois law also requires TNCs to disclose their insurance coverage to drivers and to make policy information available to injured parties who request it. If Uber Eats, DoorDash, or Grubhub is stonewalling you on insurance information, an attorney can compel disclosure through the claims process or litigation.

Who Is Liable: Driver vs. Platform

Because delivery drivers are classified as independent contractors rather than employees, the platforms generally argue they are not liable for the driver’s negligence. This is a deliberate legal shield. However, Illinois courts have recognized that in some circumstances, a platform’s degree of control over a driver’s work can give rise to liability beyond simply providing insurance coverage.

In most delivery driver accident cases, you will be pursuing:

- The driver’s personal auto insurance (if the crash occurred while the app was off, or as primary coverage in some configurations)

- The platform’s commercial policy (primary during active delivery, contingent during waiting periods)

- Both policies simultaneously if the coverage layers and the facts support it

In crashes involving serious injuries, it may also be worth investigating whether the platform’s design of the app (route demands, speed pressure, frequent notifications) contributed to the driver’s distracted driving, which could open additional avenues for compensation.

Steps to Take After a Delivery Driver Crash in Chicago

- Call 911. A police report is essential for establishing fault and documenting the driver’s employment status at the time of the crash.

- Photograph everything. Get photos of both vehicles, the crash scene, any delivery bags or equipment visible in the driver’s car, and any visible injuries.

- Ask the driver directly if they were on a delivery. Note whether they were carrying food, whether their app was visible on their phone, and the name of the platform they were using.

- Get driver and insurance information. Ask for the driver’s personal insurance card and note which delivery app was open on their device.

- Seek medical care immediately. Even if you feel fine, go to an emergency room or urgent care. Soft-tissue injuries often present hours or days after a crash.

- Do not give a recorded statement to the driver’s personal insurer or to the platform’s insurance carrier before consulting an attorney.

- Contact a Chicago car accident attorney. The overlapping coverage tiers require someone experienced in gig economy crash claims to sort out properly.

Frequently Asked Questions

Can I sue the delivery platform directly if their driver hit me?

In most cases, you will file an insurance claim against the platform’s commercial policy rather than a direct lawsuit against the company. However, if the platform’s insurer denies or underpays your claim, a lawsuit is a legitimate option. Illinois courts have addressed gig platform liability, and in some cases involving serious negligence, direct claims against the platform may be viable. An attorney can assess the specific facts of your case.

What if the Uber Eats or DoorDash driver had no personal auto insurance?

If the driver was actively logged into the app at the time of the crash, the platform’s policy applies regardless of whether the driver had personal coverage. If the driver was completely off-app and uninsured, you may need to file a claim through your own uninsured motorist (UM) coverage under your Illinois auto policy. This is one reason Illinois drivers should maintain robust UM limits.

How do I prove the driver was on a delivery when the crash happened?

Proving the driver’s app status at the time of the crash is critical. Evidence includes the driver’s own statements at the scene, any delivery bag or insulated carrier visible in the vehicle, the platform’s internal records (which can be obtained through legal process), GPS data from the driver’s phone, and restaurant or order records. Attorneys experienced in delivery driver claims know exactly what data to request and how to preserve it.

Does Illinois require delivery platforms to carry uninsured motorist coverage for injured third parties?

Illinois law under 625 ILCS 5/7-500 et seq. requires TNCs to maintain specified liability coverage during active periods. The platform policies typically do not include UM/UIM coverage for third-party claimants (people outside the vehicle). Your own UM/UIM coverage is your primary protection if the driver’s combined coverage is insufficient to fully compensate your losses.

How long do I have to file a claim after a food delivery driver accident in Illinois?

Illinois has a two-year statute of limitations for personal injury claims under 735 ILCS 5/13-202. This means you generally have two years from the date of the accident to file a lawsuit. However, you should contact an attorney as soon as possible. Evidence disappears, witnesses’ memories fade, and platform trip records may be overwritten if not preserved quickly through a formal legal hold request.

Authoritative Sources

- 625 ILCS 5/7-500 et seq., Illinois Transportation Network Providers (ilga.gov)

- Illinois Department of Insurance, Auto Insurance Consumer Resources

- 735 ILCS 5/13-202, Illinois Personal Injury Statute of Limitations

Related Illinois Injury Guides

- Rideshare Passenger Injury Claims in Chicago, Uber and Lyft Accidents

- Amazon, FedEx, and UPS Delivery Truck Crashes in Chicago

- Dealing With Progressive Insurance After a Chicago Car Crash

- Minimum Auto Insurance Requirements in Illinois, What You Need to Know

If you were injured by an Uber Eats, DoorDash, or Grubhub driver in Chicago, the coverage picture is complicated but the path forward does not have to be. Call Phillips Law Offices at (312) 346-4262 for a free consultation with a Chicago car accident attorney who handles gig economy delivery crashes.